A Famous Biscuit Brand With an Investment Portfolio Worth More Than Its Market Cap.

A sixty-year-old biscuit company. A portfolio worth more than the market cap. The business valued at zero. Buffett found the same trade in 1958. He had votes.

today I said I would publish at 4pm.

it is now past 9. wife is calling to eat.

before you read further I want to be honest about what this is and what it is not.

it is not 7FIT. it does not start with a protein bar falling out of a jacket. there is no founder parking his car. there is no bathroom epiphany at 3am. and it is definitely not a 2x in less than a year. this is a different kind of piece. longer. more analytical. some of you will find it genuinely useful. some of you will find it dry. both reactions are fair.

if I seem more serious than usual today, it is because I spent the afternoon in the hammock convincing myself I was done, and then I was not done. my wife asked why I was back at the desk. I said I was making some adjustments. she looked at the clock. she said nothing. she has learned what adjustments means.

what follows is not the thesis I was going to publish at 4pm. it is something I think is better. at minimum it is more honest. I have come to believe those are usually the same thing.

I am filing this under a new section I am calling things I wrote instead of the thing I was going to write. there is currently one entry.

do not take this as a write-up. do not take it as a sermon. take it as three months of stress I decided not to bring to the dinner table.

let’s begin.

three months in Cyprus

I spent three months researching a biscuit company listed on the alternative market of the Cyprus Stock Exchange. I read ten years of annual reports in Greek. I built a financial model spanning nine fiscal years. I mapped every position in a forty-million-euro investment portfolio buried in a segment note on page fifty-seven. I traced the ownership structure, identified a new institutional shareholder, calculated the return on invested capital of the biscuit operation separated from the holding company, and reconstructed the free cash flow from first principles using KPMG-audited data.

the result was a genuinely good investment thesis. not good in the way that investment content is usually good, compelling narrative, questionable substance. good in the way that matters: real assets, real cash flows, real margin of safety, real catalysts. the kind of thing you find once or twice a year if you are disciplined and once or twice a decade if you are lucky.

the story was perfect. a sixty-year-old biscuit company on an island in the Mediterranean. an investment portfolio worth more than the market cap. a patriarch running the business since the year Apple launched the Macintosh. the ticker symbol FBI. the annual report in Greek. a new mysterious shareholder called “Total Security.” the Sanborn Map parallel writing itself.

too perfect. that was the problem. the thesis was not just good, it was filmable. and in fifteen years of doing this, I have learned that when an investment story is too good to be true, it is usually not untrue but rather incomplete in a way that flatters the storyteller. the facts were all correct. the frame around them was not.

I could have published it as written. it would have done well. some of you would have shared it. we both would have felt smart. and the expected return of the investment would have been the same moderate, honest, unspectacular number regardless of how exciting I made the narrative around it.

so I decided to do something different. not to waste three months of work, but also not to sell you something dressed in better clothes than it deserves. instead, I am going to show you the thesis, then take it apart, then put it back together in its honest form. if you are newer to this, you may learn something about how investment narratives are constructed and why the best-looking ones are often the least reliable. if you have been doing this for a while, I hope at minimum it entertains you. and if you are looking for an actual investment, it is still a good one. just not the one I was about to sell you.

I. the company

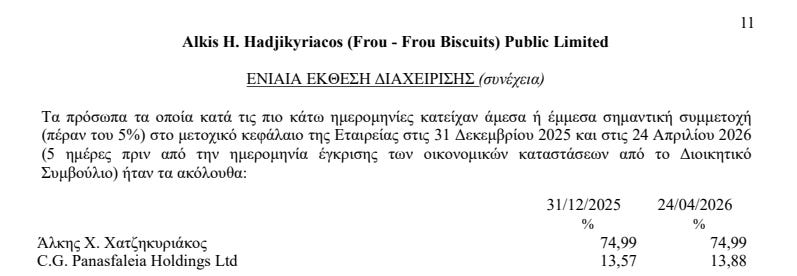

the company i want to talk about is Alkis H. Hadjikyriacos (Frou-Frou Biscuits) Public Ltd. ticker: FBI. market capitalisation: approximately forty-nine million euros. founded in 1964. its chairman, Alkis Hadjikyriacos, has been running it since 1984 and owns 74.99% of the shares.

Frou-Frou is, in economic substance, three businesses operating inside a single listed entity.

the first is a biscuit and snack operation generating twenty-five million euros in annual revenue with gross margins of thirty-nine percent, improving structurally over four consecutive years. it is the dominant biscuit brand in Cyprus, the one every child on the island has been eating since before they could read, whose crumbs have been found in locations that defy the laws of physics and basic household geography, the exclusive distributor of Cadbury and Toblerone for Mondelez International, and operates a modern factory partially powered by an 848-kilowatt photovoltaic installation. the normalised EBITDA is approximately five million euros. the free cash flow is approximately three million. there is essentially zero net financial debt.

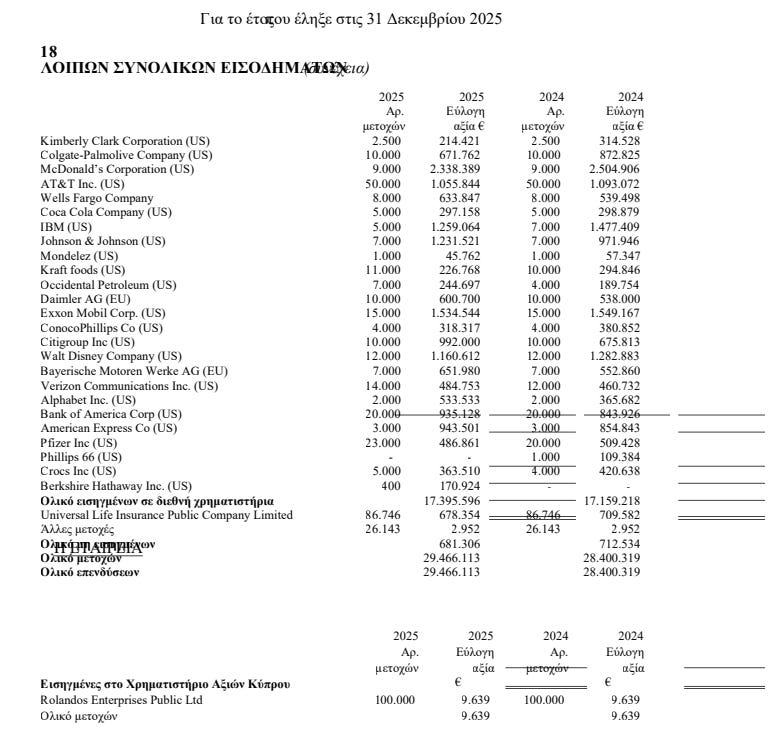

the second is a portfolio of listed securities and physical gold, held through a subsidiary called Frou-Frou Investments Limited, which has existed since 1974. the portfolio contains positions in McDonald’s, Exxon Mobil, IBM, Johnson and Johnson, Walt Disney, AT&T, Citigroup, Bank of America, American Express, Berkshire Hathaway, Vassiliko Cement Works, Atlantic Insurance, Bank of Cyprus, US Treasury zero-coupon bonds, and physical gold. at 31 December 2025, these assets were valued at forty million euros. the portfolio has compounded at approximately fifteen percent annually since 2016, with zero management fees.

the third is a collection of investment properties around Nicosia, independently appraised at ten point three million euros, in a market where property values rose fifteen percent last year.

the total equity on the balance sheet, audited by KPMG and approved on 29 April 2026, is 79.6 million euros, or eighty cents per share. the stock trades at forty-nine cents. the investment assets alone, the stocks, the bonds, the gold, the real estate, total fifty point three million euros. this approximately equals the entire market capitalisation. the biscuit business, with its five million in EBITDA and its three million in free cash flow, is being valued by the market at approximately zero.

I know what this looks like. it looks like a gift. that is why I almost wrapped it in a bow.

II. the thesis I almost wrote

the template was obvious. anyone who has spent time in value investing knows the reference.

in 1958, a twenty-eight-year-old money manager in Omaha named Warren Buffett identified a company called Sanborn Map. Sanborn produced detailed fire insurance maps of American cities. the mapping business was in structural decline, profits had fallen from over five hundred thousand dollars annually to under one hundred thousand. but the company had spent decades reinvesting its cash flows into a portfolio of stocks and bonds. by 1958, the investment portfolio was worth approximately sixty-five dollars per share. the stock traded at forty-five. the operating business was valued by the market at negative twenty dollars per share.

Buffett wrote about it in his 1960 partnership letter in a sentence that has been quoted in approximately ten thousand investment theses since: the buyer of Sanborn stock was getting the investment portfolio at a thirty percent discount with the map business thrown in for nothing.

the Frou-Frou thesis was going to follow this template exactly. investment assets exceeding the market cap. operating business valued at zero. a portfolio hiding in a footnote nobody reads, in a language most investors cannot parse, on an exchange most investors cannot find. the comparison to Sanborn was irresistible. the implied conclusion was satisfying: you, the reader, are Buffett in 1958. you have found what the market has missed. buy the stock. wait. collect your reward.

it would have been a great piece of content. it also would have been dishonest in a specific way that I want to explain, because the dishonesty is not unique to this thesis. it is endemic to a genre.

III. what everyone leaves out about Sanborn

here is what happened at Sanborn Map that the ten thousand theses referencing it almost never mention.

Buffett did not make money because the stock was cheap. cheap stocks are abundant. he made money because he had the power to force the outcome.

Sanborn’s shareholder base was dispersed. no single holder had a dominant position. the board was populated by insurance industry representatives, Sanborn’s customers, who held minimal personal stakes and whose primary interest was ensuring continued access to cheap maps, not maximising shareholder value. when Buffett identified the situation, he did not simply buy shares and wait. he accumulated twenty-three percent of the company. he allied with other dissatisfied shareholders, collectively controlling approximately forty-six percent of the votes.

Buffett obtained a seat on the board. when the incumbent directors resisted distributing the investment portfolio, Buffett threatened a proxy fight. the threat was credible because he had the votes. the directors, facing the prospect of losing their seats, capitulated. a portion of the investment portfolio was separated from the operating business and exchanged for company shares. Buffett’s partnership tendered its entire position and made approximately fifty percent.

the Sanborn investment was not a passive value bet. it was an activist intervention. the return was generated not by the market recognising the discount, which could have taken years, or never happened, but by Buffett personally wielding enough ownership to compel a specific corporate action.

this is not a minor detail. it is the entire mechanism.

IV. Generals, Workouts, and Controls

in his partnership letters from 1957 to 1969, Buffett described a taxonomy of investments that I believe is the most useful framework for understanding why some undervalued stocks generate returns and others remain undervalued indefinitely.

he divided his investments into three categories.

Generals were undervalued securities purchased at a discount to intrinsic value, where the partnership held a passive minority position. they were the largest category, typically five to six concentrated positions at five to ten percent of the portfolio, with another ten to fifteen smaller positions. the returns from Generals depended entirely on the market eventually recognising the value, an outcome Buffett could identify but could not control. he was candid with his partners: Generals moved with the overall market more than the other categories, precisely because no specific catalyst existed to force the repricing.

Workouts were event-driven investments, merger arbitrage, liquidations, reorganisations, spin-offs, where the return depended on a specific corporate action rather than on market sentiment. Workouts typically constituted thirty to forty percent of partnership assets. Buffett valued them because the returns were largely predictable and uncorrelated with the Dow Jones Industrial Average. when overall market valuations rose and Generals became scarce, he tilted the portfolio toward Workouts. when the market declined and Generals became abundant, he tilted back.

Controls were where Buffett did his most distinctive work. these were positions where the partnership acquired enough ownership to influence or dictate corporate policy. Sanborn Map was a Control. Dempster Mill Manufacturing, where Buffett accumulated seventy percent of the stock over five years, replaced the management, installed a turnaround operator named Harry Bottle, and ultimately liquidated the excess assets at a significant profit, was a Control. Berkshire Hathaway itself began as a Control, a failing textile mill purchased for its asset value.

the defining characteristic of Controls was not cheapness. Generals were equally cheap. the defining characteristic was agency, the ability to determine the outcome rather than waiting for someone else to determine it.

Buffett articulated a further insight that is directly relevant to what I am about to say about Frou-Frou. he observed that a General which declined in price could become a Control, because the falling price allowed him to accumulate a larger position until he crossed the threshold of influence. the downside of a General contained within it the option of transforming into a Control. this embedded option made Generals more attractive than a naive analysis would suggest, because the worst outcome, further price decline, created the best opportunity, accumulating enough shares to take the steering wheel.

this is, I believe, the single most important idea in Buffett’s early career, and the one most consistently ignored by people who cite his investments as precedent.

V. why Frou-Frou is not Sanborn

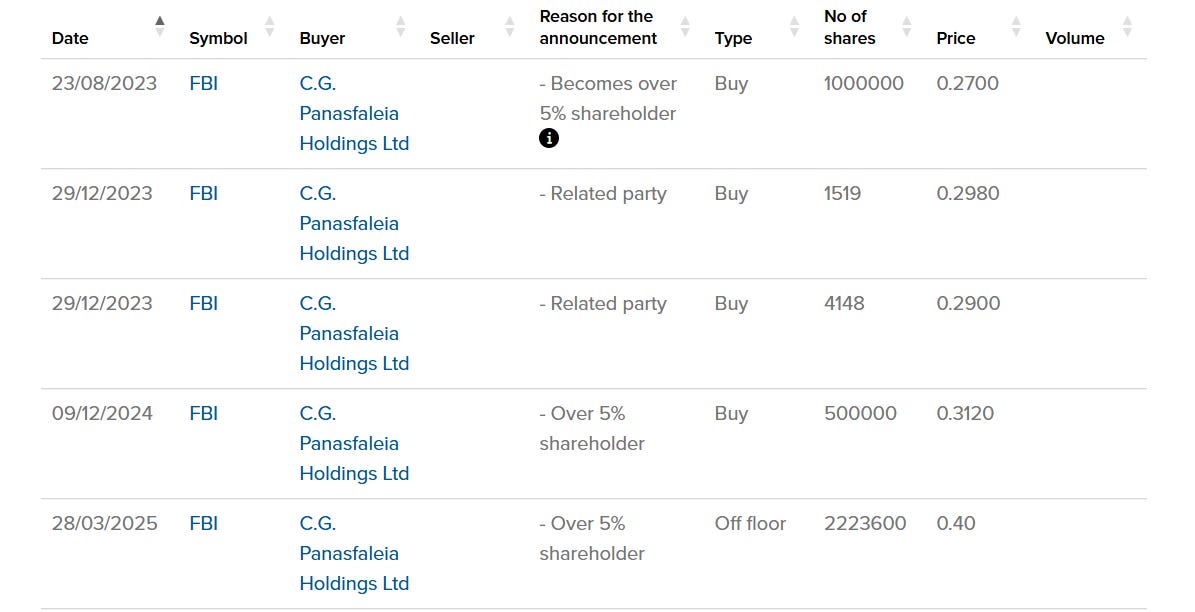

Alkis Hadjikyriacos holds 74.99% of the shares. C.G. Panasfaleia Holdings, a Cypriot investment vehicle whose name translates to “Total Security”, which I find either reassuring or ominous depending on the day, holds 13.88%. the remaining free float is approximately eleven percent.

if you purchased every available share on the Cyprus Stock Exchange, every last one, at any price, you would hold eleven percent. eleven percent against a consolidated block of seventy-five percent that has been held by one man for over four decades.

with eleven percent, you cannot convene an extraordinary general meeting under Cypriot corporate law. you cannot block any ordinary or special resolution. you cannot appoint or remove a director. you cannot force a dividend, a buyback, a special distribution, or a liquidation. you cannot do anything that Buffett did at Sanborn. what you can do is buy shares, collect whatever dividend the patriarch decides to pay, and read the annual report in Greek. I have done all three. two of them require outside help.

and critically, unlike a Buffett General, this position cannot become a Control no matter how far the price falls. the 74.99% block makes that structurally impossible. the option that made Buffett’s Generals attractive is absent here. if the stock falls, you simply have a cheaper passive position in the same company where you still control nothing.

this is the fundamental analytical error in every Sanborn comparison applied to a company with a majority controller. the comparison borrows the aesthetic of the Sanborn story, investment portfolio, discount to NAV, hidden value, while omitting the mechanism that generated the return. it is as if someone observed that birds and aeroplanes both have wings and concluded that the principles governing their flight were identical.

VI. what Buffett would actually do

the young Buffett, the partnership-era Buffett, would not buy Frou-Frou on the open market. he would not be interested in eleven percent of a company controlled by a patriarch who has demonstrated, across four decades, a preference for accumulating capital over distributing it.

what he might do is something almost no retail investor can do. he would fly to Nicosia. he would sit down with Alkis Hadjikyriacos. and he would propose a private transaction.

the economics would be straightforward. the family owns a biscuit business they have operated for sixty years and, inside the same corporate structure, a forty-million-euro investment portfolio that requires custody, regulatory compliance, currency risk management, and an annual audit. if someone offered to purchase the portfolio at a discount, say, thirty-five million for forty million of liquid securities, the family would receive cash they could reinvest as they wish, the listed company would become a pure operating entity with a simpler structure, and the buyer would acquire a diversified portfolio of blue-chip equities, sovereign bonds, and physical gold at an immediate twelve percent discount.

alternatively, a buyer could propose acquiring the entire company at a premium to market but a discount to book value. at sixty cents per share, the family would receive a forty-two percent premium to the current price while the buyer would acquire 79.6 million euros of equity for 59 million.

these are the transactions that define the best work of the value investing tradition. private. negotiated. structured so that both sides gain. they are also, by definition, unavailable to you and me. generally. they require access, reputation, capital, and the ability to write a cheque that makes a family patriarch take your call. if you are reading this on your phone at midnight considering whether to buy fifty thousand shares of FBI on the Cyprus Stock Exchange, this is not your path. your path is the open market, where you are a price-taker, a minority holder, and a passenger on someone else’s vehicle.

there is nothing wrong with being a passenger if the vehicle is going in the right direction and the ticket is cheap enough. but you should know that you are a passenger, and you should price your ticket accordingly.

VII. the value investing content machine

I have been reading investment write-ups for fifteen years.

the pattern is consistent. an analyst identifies a company trading below its net asset value. the company is typically a family holding, a conglomerate with a complex structure, or a company listed on an obscure exchange. the analyst writes a thesis. the thesis invokes Sanborn Map, or Berkshire Hathaway in 1965, or some other canonical example. there is a sum-of-parts table showing fair value at a significant premium. there is a target price. there is a disclaimer.

what there almost never is: a rigorous treatment of why the discount exists and what specific, identifiable mechanism will cause it to close.

the academic literature on holding company discounts is extensive and unambiguous. family-controlled holding companies trade at discounts to net asset value, persistently, globally, across generations. Exor, the Agnelli family vehicle, has traded at a discount for decades despite an exceptional record of value creation. Investor AB, controlled by the Wallenberg family, has traded at a discount for over a century. GBL, Jardine Matheson, CK Hutchison, Samsung C&T, the list spans continents. the explanations are structural: the costs of the holding structure itself, the private benefits extracted by controllers, the absence of minority shareholder influence over capital allocation, and the illiquidity discount inherent in concentrated ownership.

a forty percent discount on a company with 74.99% family control, listed on an alternative market with negligible daily volume, covered by zero analysts, this is not a mispricing. it is exactly what the academic literature predicts. if the stock traded at book value, that would require an explanation.

this does not mean the discount is permanent. discounts narrow when distribution policies change, when governance improves, when generational transitions shift incentives, when external shareholders accumulate positions, or when tax regimes alter the economics of returning capital. these catalysts are real, and they are, as I will discuss in a moment, present at Frou-Frou to a notable degree.

but the observation that catalysts exist is not the same as the claim that the investor controls those catalysts. at Sanborn, Buffett was the catalyst. at Frou-Frou, the investor observes catalysts that a family in Nicosia may or may not choose to activate. that is the difference between agency and hope, and it is the difference that determines whether a thesis is honest.

VIII. what Frou-Frou actually is

having explained what this investment is not, let me explain what it is. because it is, genuinely, an interesting situation, just not for the reasons the Sanborn narrative would suggest.

the honest version of the thesis is this:

Frou-Frou is a passive minority position in a family-controlled holding company where the floor is protected by fifty million euros of liquid assets, the operating business is profitable and improving, and there are documented signals, new, simultaneous, and unprecedented in the company’s history, that the family’s capital allocation policy is changing.

the floor. the investment assets, stocks quoted daily on the NYSE and CSE, US Treasury bonds, physical gold, independently appraised real estate, total fifty point three million euros. the market capitalisation is forty-nine million. the operating business generates three million in annual free cash flow independent of the portfolio. there is no debt. in any realistic stress scenario, the asset backing protects the investment. in a severe market decline, portfolio down thirty percent, the asset floor absorbs the shock and the biscuit business, which does not depend on financial markets, continues generating cash. the probability of permanent capital loss from this price is as close to zero as equity investing permits.

the return if nothing changes. the dividend has grown from 125,000 euros to 1,878,000 euros in four years and currently yields 4.4% at the market price. the portfolio compounds internally. book value grows at approximately four to five percent annually from retained earnings and portfolio appreciation. the combination produces a total return of approximately six to eight percent annually, with downside protected by the floor described above. this is the return for being a passenger while the patriarch continues doing what he has done for forty-two years.

the signals that something is changing. I will list them without embellishment, because the facts are more persuasive than any narrative I could construct around them:

the dividend has been multiplied by fifteen in four years. the company hired its first external Chief Financial Officer in 2024, who subsequently purchased shares. the fourth of five children was appointed to the board in January 2026, the next generation now holds six of twelve seats. in December 2025, 16.3 million euros of the investment portfolio was reclassified from long-term to current assets, accounting terminology meaning the company expects to convert them to cash within twelve months. for the first time in the company’s history, the annual report contains the sentence: “in 2026, the Board may proceed with the liquidation of a specific number of investments depending on the prevailing market conditions.” the share buyback has been authorised by shareholders in three consecutive years. an external value investor, C.G. Panasfaleia Holdings, has accumulated 13.88% of the capital, representing approximately fifty-five percent of the available free float, without making any public demands. and the Cypriot parliament, effective January 2026, reduced the tax on dividends from seventeen percent to five percent.

none of these facts existed three years ago. all of them exist now. simultaneously.

and one of them deserves more than a bullet point.

C.G. Panasfaleia Holdings has accumulated 13.88% of this company, representing approximately fifty-five percent of the available free float. they did not do this passively. they paid more each time they bought. they cannot exit through the market without destroying the price. their only path to a return is internal value realisation. that is not a passive investor waiting for the market to wake up. that is a concentrated, sophisticated shareholder whose entire incentive structure is aligned with minority holders and who is visible to management at every board meeting and every general assembly.

and the 16.3 million euros reclassified to current assets, combined with the explicit written declaration of possible liquidation in 2026, is not a signal that the market might eventually notice something. it is a management team stating publicly, in a KPMG-audited document, that they are preparing a specific action in a specific timeframe.

that is closer to a Workout than a General. the mechanism is documented. the timeline is stated. you do not control the outcome. but the situation has a shape that generic holding company discounts do not have.

these are not the same as waiting for a market to recognise a discount. but they are also not a guarantee. the fundamental difference between this and Sanborn is that Buffett was the catalyst. here, the catalyst is a family in Nicosia that appears to be moving in the right direction, for the first time in forty years, simultaneously, with eight documented signals that did not exist three years ago.

appears. moving. the qualifying words are doing real work in that sentence.

if the discount closes it will be because a family decided to close it. not because you forced anything. not because the market woke up. because Alkis Hadjikyriacos, or his children, or the pressure of a 14% external shareholder, produced a decision that you have no vote on and no leverage over.

that is the honest version of the thesis. the direction looks right. nobody is guaranteeing the destination.

the return if the discount compresses. if the family’s distribution policy continues to evolve, if dividends keep growing, if the buyback is executed, if any portion of the reclassified assets is distributed, the holding discount should narrow from approximately forty percent to approximately fifteen to twenty percent. this is the normal range for holding companies that actively return capital. the resulting re-rating would generate approximately thirty to forty percent of price appreciation over two to four years, on top of the growing dividend. total return in this scenario: approximately twelve to fifteen percent annualised.

this is not a spectacular return. it is not a five-bagger. it will not change your life. but it is a legitimate, well-protected, double-digit total return in an asset with near-zero risk of permanent capital loss, and that combination is genuinely rare.

IX. on choosing honesty over engagement

I could have written the original thesis. the Sanborn comparison. the portfolio hidden in Greek. the biscuit business at negative seven million. the target price at sixty-eight cents. it would have been shared. it would have generated engagement. it would have been, in the parlance of the industry, a “great write-up.”

and the expected return of the investment would have been exactly the same.

the difference would have been in what the reader believed they were buying. the exciting version sells a mispricing, a market error waiting to be corrected, Sanborn 2.0, fifty percent upside. the honest version sells a well-protected moderate compounder with asymmetric optionality, six to eight percent if nothing changes, twelve to fifteen if catalysts activate, near-zero probability of permanent loss.

both versions describe the same company. they describe different relationships between the investor and the truth.

I do not think the value investing community has a dishonesty problem. I think it has an incentives problem. the format rewards drama. the audience rewards conviction. the platform rewards engagement. and the easiest way to generate all three is to find a stock that looks like Sanborn, write it up as though it were Sanborn, and move on before anyone checks whether the discount closed.

nobody publishes the follow-up article two years later titled “the Discount Did Not Close and Here Is What I Learned.” that article does not get engagement. it does not get you invited to conferences. it makes you look like you were wrong. the structural incentive is to publish theses and never revisit them, to cite Buffett and never mention that Buffett had the power to force what we can only suggest, and to conflate the identification of value with the ability to realise it.

I have three months of research on this company. throwing it away seemed wasteful. packaging it as something it was not seemed worse. what remains is this: an honest piece about a good investment and an honest industry that has an unfortunate habit of dressing moderate opportunities in spectacular clothing.

if you are early in your journey, I hope the distinction between Generals and Controls, between agency and observation, between narrative and mechanism, is useful. these are the ideas I wish someone had explained to me fifteen years ago with a real example and without the pretence that every undervalued stock is a catalyst waiting to happen.

if you have been doing this for a while, I hope at minimum you found the biscuit company entertaining. someone in Nicosia is selling covered puts on NYSE stocks inside a Greek-language annual report for a company that makes digestive biscuits. the same digestive biscuits that have been generating crumbs on Cypriot sofas, car seats, and laptop keyboards since 1964. the world is a remarkable place.

and if you are looking for an actual investment, it remains a good one. not the one I was going to sell you. a better one, because you know exactly what you are buying and what you are not.

I hold a small position in this company. it sits in the part of my portfolio I think of as safe rather than aggressive, capital I am comfortable compounding at six to eight percent annually while I wait for something I cannot control to happen or not happen.

that is the most honest sentence I have written about this investment.

if the catalysts activate I will have been right for the right reasons. if they do not I will write about that too.

X. the rating:

“the map and the biscuit, the same trade, same page

but buffett had votes and we only have age

the floor is in dollars, the ceiling in greek

the direction looks right, but nobody can speak”

- DCE

wednesday I will write about a spanish company. I met management in person less than two weeks ago. my base case is a double in two years.

it starts with a better story than biscuits.

see you then.

this is not financial advice. the author holds shares in Alkis H. Hadjikyriacos (Frou-Frou Biscuits) Public Ltd and may buy or sell at any time. the stock is extremely illiquid. the annual reports are in Greek. all financial data is sourced from the KPMG-audited FY2025 annual report approved 29 April 2026. zero analysts cover this security. confirm all data independently before making investment decisions.

This was really well done! Your writing style is engaging and accessible, regardless if the reader is an experienced investor, has finance expertise, or simply a layperson. There’s valuable lessons in honesty, patience, divergent and critical thinking, all presented in an easy, flowing style. I’m impressed and looking forward to reading more. Thank you, it was kind of inspiring.

The only negative: you make reading annual reports sound fun, almost cool. Ha!

Good. I liked the part about control. Too many writers forget about such a tiny nuance.